The Effect of Moderated Premiums on Small Employers

Sandy Fester, VP of Middle and Small Group Business

| 3 min read

Sandy Fester is vice president of Middle and Small G...

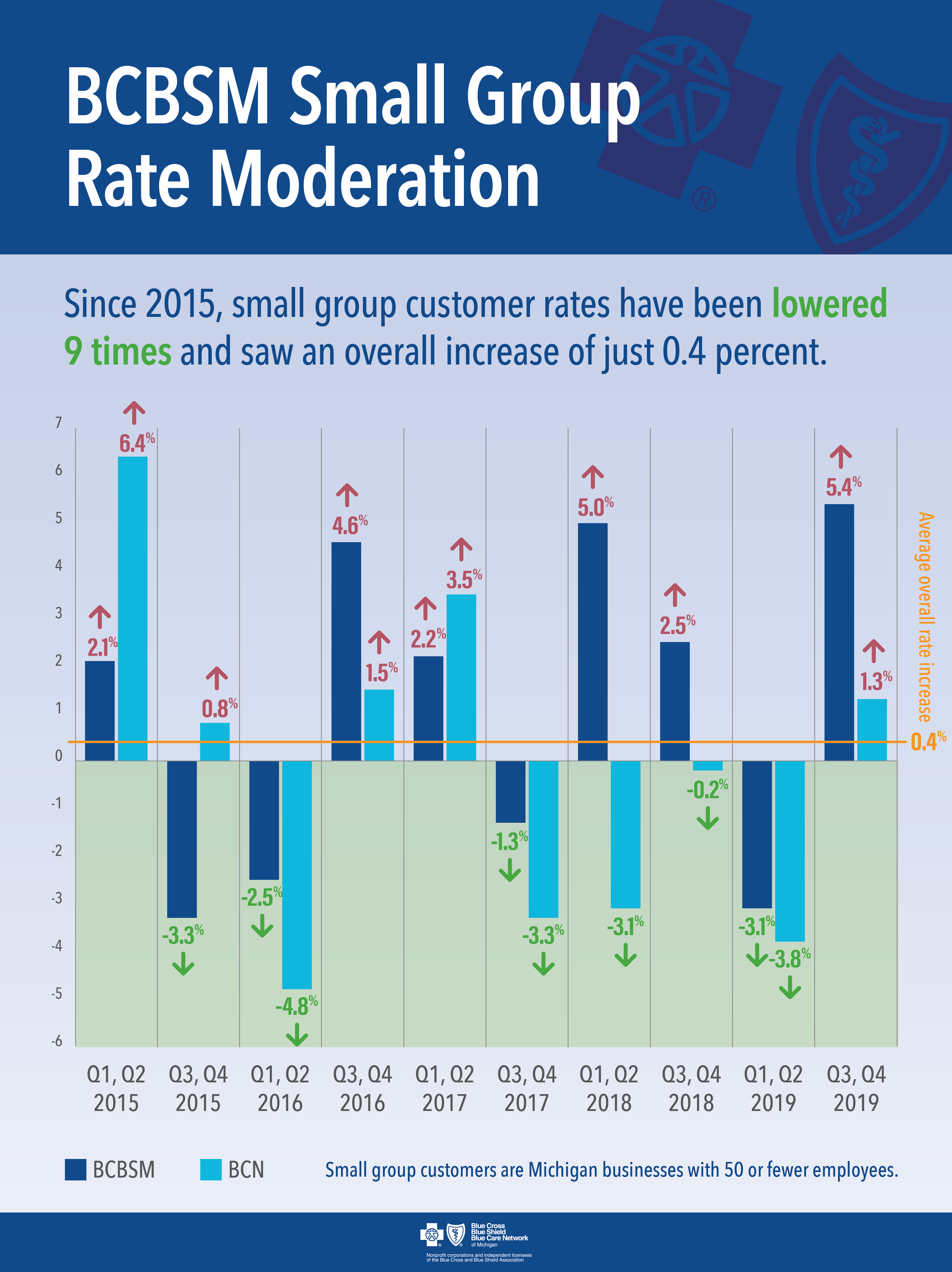

Is health coverage a “nice to have,” or a “must have” benefit for small businesses to provide employees? At Blue Cross and Blue Care Network, we recognize the “must have” expenses for small business owners – rent, utilities, payroll, taxes – certainly can push health and dental benefits to the sideline. We are working hard to make sure that isn’t the case, and that owners of small businesses have affordable options and predictable costs for employee health care. In fact, we’ve lowered our statewide average rates for small employers nine times since 2015. Even more importantly, we’ve kept costs for health insurance within a predictable range of increase of between 0 and 1 percent over that time.

Predictable costs allow business owners to plan effectively, and provide health benefits their employees see as critical. In fact, 66 percent of recruiters say medical and dental coverage is the most important perk for recruiting and retaining the best job candidates.

Still, only 33 percent of Michigan’s small businesses provided employee health benefits in 2017. A 2019 study shows 45 percent of small business owners make coverage decisions based on premium affordability.

This data reaffirms the importance of Blue Cross’ continuous work to moderate premiums and keep coverage affordable for small businesses – and we’re proud of the ongoing results we’ve seen. Blue Cross calculates new rates for our small business members twice every year. In the first and second quarter of this year, we were pleased to offer an average rate reduction across the board for PPO and HMO products – 3.1 percent and 3.8 percent lower premiums, respectively. For the third and fourth quarter of this year, we’re anticipating a moderate increase of 1.3 percent for HMO and 5.4 percent for PPO members. This means that since 2015, PPO members have seen an overall rate increase of just over one percent, while HMO members have experienced a decrease of just under one percent. Combined, our small business customers have received a modest rate increase of only 0.4 percent over the last five years – less than ½ a percent. Blue Cross’ rate changes in Michigan are far below those seen nationally since 2015.

So, how do we plan to continue to promote the predictability of health insurance costs? For more than a decade, Blue Cross has focused on the root causes of health care costs by working with Michigan’s best doctors and hospitals to implement health care efficiencies and improve patient outcomes. We’ve also designed programs to enhance member well-being and convenient access to care such as Virtual Well-Being and telehealth options.

By continuing to address the cost drivers that affect insurance rates, we at Blue Cross remain focused on giving Michigan employers what they need – affordability and predictability – and helping them make the decision to provide health benefits that surveys show will make them stronger, and help their businesses grow. Interested in learning more? Reach out to a Blue Cross independent agent at www.bcbsm.com.

{kind=link}